The Future of Cell Towers and Leases

By Ken Schmidt, Steel in the Air

I have been advising landowners, tower companies, investors, and analysts in the wireless infrastructure industry for more than 22 years. In that time, I have watched the industry evolve through multiple technology cycles, two major consolidation waves among wireless carriers, the birth and near-death of small cells as a macro tower replacement, and the slow-motion transformation of what was once a high-margin, relationship-driven business into something that increasingly resembles a commoditized utility.

I have been thinking about the long-term future of cell tower leases for most of those 22 years. I have advised funds, analysts, and tower companies on these questions. What follows is my honest assessment — not a promotional piece, not a list of reasons to panic, and not a reassurance that everything will be fine. It is an attempt to think clearly about a set of forces that are genuinely complex and, in some cases, moving faster than the industry acknowledges.

I am a generalist. I know the lease side of this industry as well as anyone. I know carrier motivations, tower company economics, and the landowner’s position at the bottom of the information hierarchy better than most. On the technology side — particularly AI — I have views, but I hold them with appropriate humility. I am genuinely interested in pushback from people who know more than I do on those dimensions. More on that at the end.

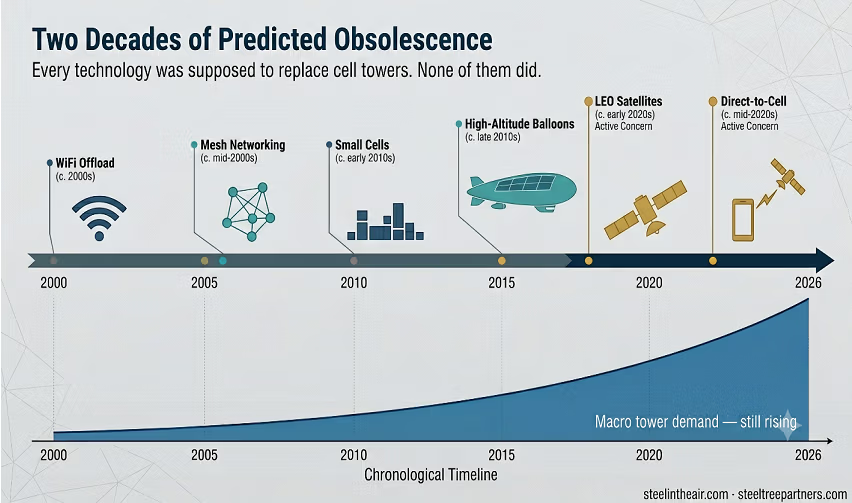

The Threats We Have Heard Before

Every few years, a new technology arrives that someone (typically lease buyout or lease optimization companies) claims is going to make cell towers obsolete.

- Small cells were going to replace macro towers by handling density in urban markets so efficiently that large towers would become redundant. They didn’t. They supplemented macro infrastructure, and in most markets outside of a handful of dense urban cores, the economics never penciled out without the fiber backhaul that most tower companies didn’t own.

- High-altitude platforms — Google’s Loon being the most visible — were going to provide coverage over remote areas without towers. Loon is gone. The physics of providing reliable, high-capacity wireless coverage from a moving platform proved more complicated than the press releases suggested.

- Mesh networking was going to allow devices to route around towers entirely. It remains a niche technology for specific industrial and military applications.

- Satellites were always the most credible long-term threat, and they remain so — though not for the reason most landowners cite. I’ll return to that.

The pattern across all of these is the same: promising technology, genuine capability in specific use cases, real pressure on the margins of macro tower economics — but no displacement of the core macro infrastructure. The reason is physics. Mid-band spectrum, where 5G capacity lives, propagates roughly half as far as low-band spectrum. Sites engineered for 1.9 GHz need to be supplemented — not replaced — to deliver meaningful mid-band 5G coverage. That dynamic actually increases the number of sites required, not decreases it.

History doesn’t guarantee the future. But it does establish a directional pattern that deserves respect.

What Landowners Ask Us About Most

When we talk to landowners, the questions cluster predictably. Satellites are by far the most common concern — driven in no small part by aggressive marketing from lease buyout companies that have used satellite-to-cell anxiety to pressure landowners into accepting lower valuations. Advances in technology generally are a close second. Small cells are a distant third; most landowners have internalized by now that small cells complement macro towers more than they threaten them.

The satellite concern we take seriously is different and more subtle. It is not a replacement. It is the erosion of pricing pressure. Just last week, AT&T’s stock dropped 13% partially or entirely) due to the fear of price erosion from Starlink and others.

As of early 2026, SpaceX’s Starlink has more than 650 direct-to-cell satellites in orbit and launched T-Satellite commercially with T-Mobile in mid-2025, initially offering text messaging in areas with no cellular coverage, with data following by late 2025. This doesn’t threaten a suburban macro tower. But in very rural areas — where the carrier’s “Plan B” has historically been nonexistent — satellite now provides a genuine alternative for low-bandwidth, non-latency-critical applications. The carrier no longer has to maintain an expensive rural site to say it has coverage there. The site doesn’t get terminated immediately. It gets renegotiated downward. That is the slow-bleed scenario, and it is already beginning in the most marginal rural markets.

Elon Musk is also a specific risk factor worth naming plainly. His behavior in markets he enters is frequently disruptive in ways that don’t follow conventional commercial logic. SpaceX’s acquisition of EchoStar’s spectrum assets bolsters its position and ambition in the direct-to-cell space. Rational competitive analysis has limited predictive value when one participant operates outside normal commercial constraints.

What Actually Keeps Us Up at Night

The threats that concern me most are not the ones landowners ask about. They are structural, slower-moving, and harder to see from the landowner’s position.

The Commoditization of Wireless

Wireless in the United States is functionally a three-carrier oligopoly competing primarily on price, bundling, and brand. The product — connectivity — is increasingly indistinguishable between providers. When a product becomes a utility, every party in the supply chain faces sustained margin compression. Carriers pass that pressure on to tower companies through master lease negotiations. Tower companies push it onto landowners through rent-reduction campaigns, lower escalators in new leases, and prepaid buyout offers designed to remove future escalation exposure from their books.

This is not a new dynamic, but it is accelerating. The wireless market’s shift from four carriers effectively to three — with T-Mobile absorbing US Cellular assets and AT&T and SpaceX acquiring DISH’s spectrum — removes the competitive pressure that historically forced carriers to move quickly and pay fairly. New cell tower lease proposals in 2026 are lower on a straight-dollar basis than in prior years, with lower escalation rates and more unfavorable terms across the board. The 2% escalator cap — once a negotiating floor — is now frequently a ceiling, and some developers are pushing for less. Even a 0.5% difference in escalator represents five figures in lost value over a 25-year lease.

The Competitive Dynamics Among Tower Companies

I want to be precise here because the framing matters. Some of what looks like poor decision-making by tower developers — accepting punishing master lease terms, building near existing towers, agreeing to large equipment buckets, accepting claw-back provisions on future collocator revenue, committing to sub-2% escalators — is not always poor decision-making. In some cases, it is a deliberate competitive strategy by well-capitalized players.

A large private tower company with access to cheap capital and a portfolio of thousands of sites can absorb master lease terms that would be existential for a smaller competitor. When a carrier demands a claw-back on collocator rent, a sub-2% escalator, and a large equipment footprint at minimal additional rent, the big player takes the deal and survives on scale. The 50-tower developer does not. The result is accelerated consolidation, fewer but more compliant tower partners for carriers, and a continued race to the bottom in the terms that ultimately flow through to ground-lease economics.

The landowner is at the end of that chain. Tower buyers in 2026 are paying close attention to which carriers anchor a tower and the pace of historical lease-up — and they are applying more discipline than ever to assets they consider structurally compromised. The market is getting better at distinguishing strong assets from convenient ones, and the gap between their valuations is widening.

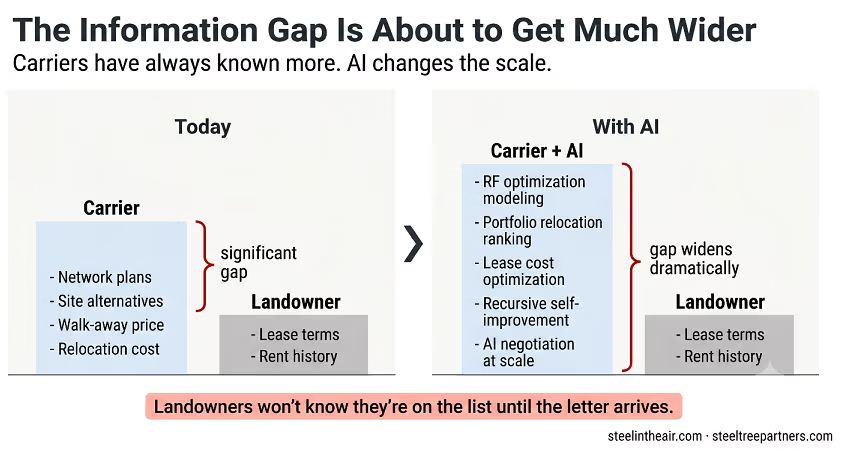

AI — The Growing Information Gap

This is the threat I think about most, and the one the industry is least prepared to discuss honestly.

Carriers have always had a significant information advantage over landowners. They know their network plans, their alternatives, their walk-away points, and the relative value of every site in their portfolio. Landowners typically know none of this. That asymmetry is the reason firms like ours exist — to narrow the gap on behalf of the people who own the land.

Artificial intelligence is about to widen that gap dramatically.

The version of AI that concerns me is not chatbots drafting lease counteroffers — we have already written about why that is dangerous for landowners. The version I am concerned about is recursive, self-improving AI applied to network and portfolio optimization. Systems that can simultaneously evaluate RF propagation models, zoning barriers, terrain, traffic demand, lease costs, and relocation feasibility — iterating continuously, correcting their own errors, improving with every cycle. These systems don’t just identify which sites are overpriced. They rank them, model the cost of relocation against the cost of continued lease payments, and generate a prioritized action list.

Carriers and large tower companies are investing in exactly this capability. The landowner sitting on a site that scores poorly on that model will receive a renegotiation request or a termination notice. They will have no idea they were on the list until it arrives.AI negotiation with landowners is coming too. The same technology that can optimize a network portfolio can conduct initial lease negotiations — patiently, consistently, at scale, without the need for a human on the other end. We are not there yet. We are closer than most people think.

The information asymmetry between landowners and carriers has always been wide. AI will widen it further and faster than any previous technology. That concerns me more than satellites.

The FCC’s Siting Proposals

In September 2025, the FCC adopted a Notice of Proposed Rulemaking under its “Build America” agenda proposing to streamline wireless infrastructure deployment by reducing state and local regulatory barriers. The NPRM proposes reforms that would override state and local authority over the siting, modification, and renewal of wireless facilities — expanding eligible facilities requests under Section 6409, limiting local fees, and constraining zoning-based objections to new infrastructure.

This matters for landowners because zoning complexity is a meaningful source of leverage. When a carrier or tower company cannot easily relocate a site due to permitting timelines, historic preservation requirements, or local opposition, the landowner has negotiating power. If federal preemption materially reduces those barriers, some sites currently protected by zoning friction become easier to replicate or relocate.

The NPRM is not yet final. Local governments have filed substantial opposition. But the direction is clear, the carrier industry’s support is unified, and the current FCC administration is explicitly motivated to reduce what it calls unlawful barriers to deployment. Landowners who are counting on zoning complexity as their primary source of leverage should be paying close attention.

Satellites — Pricing Floor Erosion, Not Replacement

Already addressed above, but worth restating as a structural concern: in rural markets, satellite now provides carriers with a credible “good enough” coverage alternative for low-value use cases. That changes the negotiating dynamic at the margin — not catastrophically, not quickly, but directionally and persistently. The very rural site that was previously irreplaceable may now have a satellite-shaped Plan B that didn’t exist three years ago.

What Makes Us Optimistic

The industry has been predicting the obsolescence of macro towers for as long as I have been in it. The towers are still there. That alone should be instructive.

1. Physics Doesn’t Change

Mid-band 5G requires more sites, not fewer, to cover the same geography as legacy low-band networks. AT&T and Verizon are still in the middle of their mid-band buildouts, chasing T-Mobile’s spectrum position. That is near-term, concrete, site-driven demand. It doesn’t require any optimistic assumptions about AI or IoT. It just requires AT&T and Verizon to compete — which they will.

2. The Data Growth That Actually Matters

The wireless industry frequently cites mobile data growth statistics to support bullish infrastructure arguments, and those numbers deserve serious scrutiny. A significant and underappreciated portion of recent mobile data growth has been driven by Fixed Wireless Access — carriers deploying FWA broadband services using spectrum and network capacity that was already built and largely sitting fallow. FWA consumes existing network capacity rather than requiring new infrastructure investment. It should not be weighted anywhere near the same as genuine mobile demand growth when evaluating future tower economics, and the industry routinely fails to make that distinction.

The demand growth that actually drives tower economics is genuine mobile and nomadic traffic — handsets, mobile video, connected vehicles, and the emerging categories discussed below. That growth is real, but more modest than the headline numbers suggest. Investors and landowners should be skeptical of analyses that lean on aggregate mobile data figures without carving out the FWA component.

3. True IoT — The Underappreciated Demand Driver

This is where I am genuinely optimistic about long-term macro demand, and where the industry discussion remains the least developed.

Connected IoT devices are expected to approach 40 billion globally by 2030, up from roughly 21 billion in 2025. Most of that growth is in Wi-Fi and Bluetooth — indoor, static, low-mobility applications that don’t require macro wireless infrastructure. But a meaningful and growing subset requires terrestrial cellular connectivity: autonomous vehicles, mobile robotics, connected agricultural equipment, nomadic industrial sensors, emergency response systems, and any application where latency is critical and the device moves.

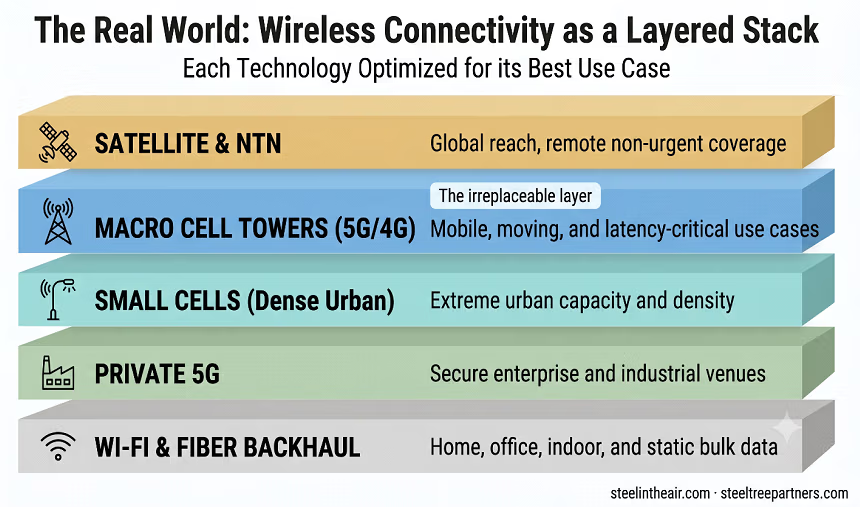

Satellite cannot serve these applications at scale. The latency constraints on autonomous vehicles are measured in milliseconds. Satellite, even LEO, cannot (yet) reliably deliver that, especially at the scale necessary. For latency-critical, mobile use cases, terrestrial macro wireless is not one option among several — it is the only option.The connectivity stack that will emerge is layered: Wi-Fi and fiber for indoor static applications; terrestrial cellular for mobile and latency-critical uses; satellite for mid-latency, non-urgent applications in remote areas; and private 5G for large venues and enterprises. Macro towers are the backbone of the cellular layer. That layer is not going away.

4. AI as a Demand Driver — With Appropriate Uncertainty

There is an active, genuinely unresolved debate in the industry about how AI affects wireless network demand. The bull case: AI inference — the real-time application of trained models to generate outputs — increasingly happens at or near the network edge rather than in centralized data centers. Applications such as real-time video analysis, augmented reality, and agentic AI systems that interact with the physical world require low-latency edge compute proximate to the tower. Critically, many of these applications are upload-heavy in ways that existing networks were not designed for. The network asymmetry built for download, not upload, becomes a constraint as AI workloads mature.

The bear case: on-device AI processing handles more and more locally, reducing the need to send data to the network at all. AI systems are becoming better at determining which information needs to leave the device and which doesn’t, thereby suppressing demand rather than generating it.

Both are plausible. I am not going to pretend to know which wins. What I will say is that American Tower, in its recent earnings calls, has identified AI inferencing as its fastest-growing new use case in its data center business, which suggests the edge compute buildout is real, even if the tower-level implications are still developing. The WIA indicates that AI traffic now accounts for 4.2% of total wireless network traffic (although they don’t indicate whether they include AI traffic on Fixed Wireless Access or not, which is a meaningful distinction). And the sectors most likely to drive wireless upside — AR/VR, autonomous systems, mobile robotics — are structurally dependent on terrestrial wireless, regardless of how the on-device AI question is resolved.

5. The Track Record

Two decades of predicted obsolescence. The towers are still there. The leases are still being paid. The industry is more concentrated, the terms are harder, and the information gap is wider — but the fundamental asset endures. That is not a reason for complacency. It is a reason for calibrated confidence about underlying macro demand, paired with serious attention to the specific characteristics of individual sites.

The Sites That Are at Risk

Not all towers are equal, and the definition of what makes a site valuable is changing. In our view, the following categories face the most meaningful risk over the next decade:

High-rent sites that can be relocated. If a carrier or tower company can replicate your site’s coverage from an adjacent property at lower total cost, they will eventually try. The question is always whether your specific location is genuinely irreplaceable to the network — or just convenient. Tower buyers in 2026 are already applying more scrutiny here than at any point in the recent past.

Shorter structures in urban and suburban markets. Some will face pressure from small-cell and mid-cell densification, particularly if the FCC’s proposed siting reforms reduce the friction in deploying small cells on public rights-of-way.

Very rural sites. The most marginal rural sites face the combined pressure of satellite alternatives for low-bandwidth coverage, high operating costs, and limited collocator demand.

High-opex sites. Rent is only part of what a carrier or tower company evaluates. Sites that are difficult to access, costly to maintain, or require frequent structural remediation are candidates for relocation, even if the rent is reasonable. Total cost of ownership is what gets evaluated, not rent in isolation.

DISH and US Cellular tenanted towers. As noted in our analysis of how 2025 reshapes tower ownership, DISH leases are already being valued at a fraction of comparable agreements with the Big Three, and the risk of near-term termination is real. Tower owners in this position need to understand exactly where they stand before that risk materializes.

The Sites That Retain Their Value

Unique sites are still unique. A hilltop with a clear line of sight in a market where alternative locations require rezoning, environmental review, and years of permitting is not a commodity. A rooftop in a dense urban market, with anchor-tenant equipment and no viable structural alternative, is not easily replaced. Towers with multiple collocators, long remaining lease terms, and locations that serve genuine network coverage gaps — not just capacity redundancy — retain meaningful value.

The carriers need more density, not less, particularly AT&T and Verizon, as they continue their mid-band buildouts. That demand is real and site-specific. It benefits the right sites meaningfully.

The risk is not that macro towers become worthless. The risk is that the industry increasingly separates into two tiers — sites that are genuinely irreplaceable and sites that are merely convenient — and that the treatment of those two tiers diverges sharply over time. What buyers want in 2026 reflects that divergence: more competition for the right assets, more discipline around the wrong ones.

What kept a lease healthy in 2010 may not be sufficient in 2030.

What This Means for Landowners and Investors

The industry is at an inflection point. The structural forces — commoditization of wireless, AI-driven information asymmetry, erosion of some zoning protections, deliberate consolidation dynamics among tower companies — are not temporary. They are directional. And they are moving faster than most landowners realize.

Smart landowners and investors are taking a more critical look at their assets. Not in panic, but with the same analytical rigor that carriers and tower companies have been applying for years. Every lease and every tower should be evaluated on three dimensions simultaneously:

Short-term: Is the current rent at or near fair market value? Are the escalation terms competitive? Are there near-term renegotiation requests or prepaid offers that require a response? For context, cell tower leases currently trade at 15x to 25x annual rent, and towers at 15x to 40x tower cash flow — but those multiples vary significantly based on tenant quality, lease terms, and site characteristics. Knowing where you fall in that range matters.

Mid-term: What is the site’s utility to the specific carrier or tower company occupying it? Does the network need this specific location, or is it one of several viable alternatives? Is the site at risk of renegotiation or termination as AI-driven portfolio optimization becomes more sophisticated?

Future-facing: Is this site’s location unique enough — topographically, logistically, from a zoning standpoint — to remain valuable as the definition of a “good site” continues to evolve? Does it sit in a market where demand for densification is likely to grow? Or is it in a category — very rural, high-opex, easily relocated — that faces structural headwinds?

Most of our competitors are focused on the short-term question alone. Some address the midterm. Almost none are asking the future-facing question systematically.

A Note on What I Don’t Know — and an Invitation

I want to be direct about the limits of this analysis. I know the lease and landowner side of this industry with confidence, built over 22 years, backed by a proprietary database of more than 17,000 lease rate data points. I know carrier motivations and tower company economics well enough to be appropriately skeptical of both when they conflict with landowner interests — which is often.

On the technology side — particularly AI network optimization, recursive learning systems, and the evolution of edge inference — I have views, but they are those of an informed generalist and avid user, not those of a technical specialist. If you know more than I do about AI-RAN, self-optimizing network systems, on-device inference trends, or the actual upload/download demand profile of emerging AI applications, I genuinely want to hear from you. That includes if your analysis contradicts mine. The best thinking in this industry has always come from people willing to say what they actually believe, not what confirms existing narratives.

Good sites are still good sites. But knowing whether you have one — and whether you will still have one in ten years — requires asking harder questions than most people in this industry are currently asking.

If you own a tower or a lease and want to think through where it sits across all three time horizons, Steel in the Air and SteelTree Partners are the places to start.

Don't navigate this alone

Ken Schmidt is the founder of Steel in the Air, a cell tower lease advisory firm, and a principal at SteelTree Partners, a cell tower and lease brokerage. Both firms work exclusively on behalf of landowners, building owners, and tower owners.